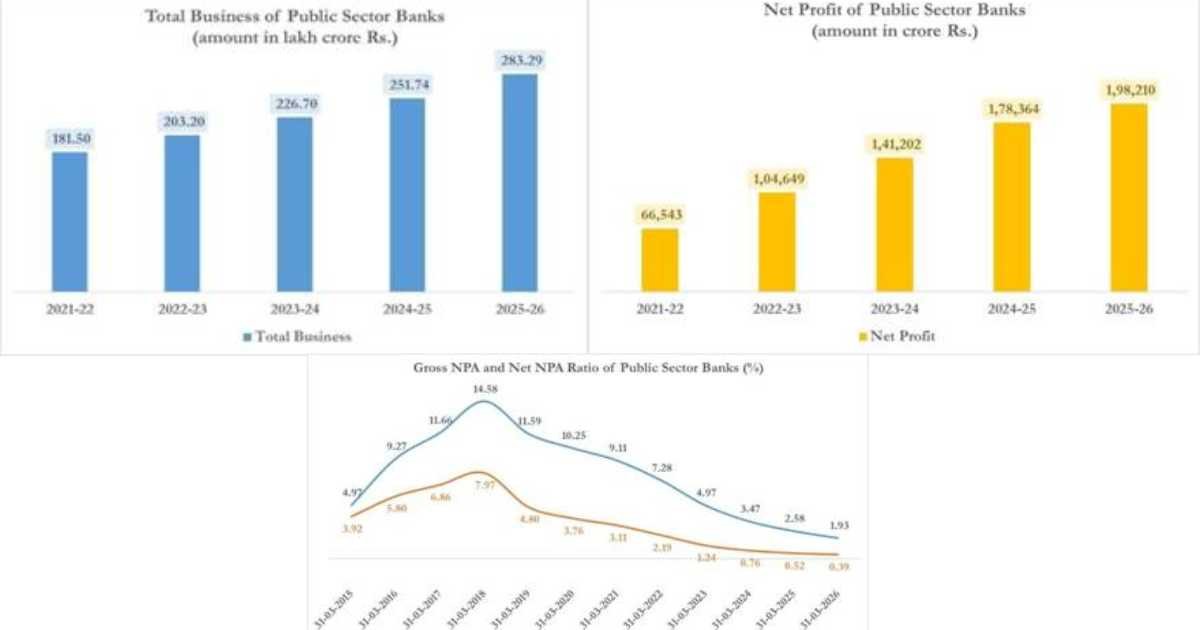

New Delhi: Public Sector Banks (PSBs) recorded a historic PSB net profit of ₹1.98 lakh crore in FY 2025–26. This marked the fourth consecutive year of overall profitability. Moreover, the performance reflected stronger balance sheets and sustained reforms.

The combined business of PSBs reached ₹283.3 lakh crore as of 31 March 2026. This represented 12.8% year-on-year growth. In addition, deposits rose 10.6% to ₹156.3 lakh crore, showing continued public confidence.

Gross advances increased 15.7% to ₹127 lakh crore. Credit demand remained strong across sectors. Furthermore, retail, agriculture and MSME lending expanded at a healthy pace.

Retail advances grew 18.1%. Agriculture loans rose 15.5%. MSME credit expanded 18.2%. Consequently, PSBs continued to support financial inclusion and entrepreneurship.

Asset quality improved significantly during the year. The Gross NPA ratio fell to 1.93%. Meanwhile, the Net NPA ratio declined to 0.39% as of 31 March 2026. These levels marked historic lows.

PSB net profit supported by strong asset quality and capital position

The improvement in asset quality strengthened overall stability. Each PSB maintained provisioning coverage above 90%. Therefore, banks demonstrated prudent risk management and stronger underwriting standards.

Fresh slippages declined further. The slippage ratio reduced to 0.7%. In addition, total recoveries reached ₹86,971 crore. This included recoveries from written-off accounts.

Higher income and better recovery mechanisms boosted profitability. Aggregate operating profit stood at ₹3.21 lakh crore. As a result, PSB net profit reached ₹1.98 lakh crore.

Capital adequacy remained comfortable. The aggregate CRAR improved to 16.6% as of 31 March 2026. Banks also raised ₹50,551 crore in capital during the year. Moreover, CRAR levels stayed well above the regulatory requirement of 11.5%.

Operational efficiency improved as well. The cost-to-income ratio declined to 49.67%. Technology adoption and digital initiatives supported this improvement.

Officials said continued reforms, stronger governance and enhanced credit discipline contributed to the results. Therefore, PSBs now operate with healthier balance sheets and greater resilience. They remain well positioned to support economic growth and credit demand.